The Horizon Europe project offers a variety of funding models to support project implementation, the most common are the Actual Costs and Lump Sum models. While the Actual Costs model is based on the reimbursement of actual expenses, the Lump Sum model consists of a predetermined budget.

The Lump Sum model was introduced in 2018 to simplify the management of EU-funded projects, changing the focus from financial management to the technical aspects of the project. While under Horizon Europe, its use has become more prevalent, there is still some reluctance to adopt this model, as it requires a different approach during the proposal preparation and is often seen as complex.

In this article, we will compare these two funding schemes, reviewing their benefits and challenges, contributing to an informed decision.

Actual Costs

For several years, the Actual Costs model was the primary funding scheme used in EU-funded projects. During the project proposal preparation, funding is distributed between partners based on their involvement in the action and divided between cost categories. Before the project begins, a pre-financing payment is made by the granting authority. Throughout the project execution, beneficiaries are required to keep records of all their expenses and supporting documentation organised by cost categories. At each reporting period (RP), the beneficiaries submit a report of their spending to receive the interim payments. This model depends on audits to ensure transparency and compliance with the funding guidelines.

Lump Sum

Under the Lump Sum model, funding is allocated based on predefined budgets defined per work packages (WP). Milestones, deliverables and WP objectives must be meticulously planned and defined to ensure they are achieved before the end of each RP. Similar to the Actual Costs model, at the beginning of the project, the beneficiaries will receive a pre-financing payment (if foreseen in the call). However, during the project execution, instead of reporting expenditures per cost categories, beneficiaries are required to complete their milestones and deliverables as outlined in the Grant Agreement. Interim payments are made upon review meetings that confirm that work package activities have been completed. This model eliminates the need for detailed financial reporting and audits, reducing the administrative burden during the project execution.

However, audits to non-financial aspects of a project (e.g. results, IPR, research integrity, ethics) are still possible and, in extraordinary cases, a financial audit project may occur, as this is still foreseen in the Grant Agreement. We advise you to keep standard accounting records and tax reports, complying with the obligations outside the grant agreement, such as national law and internal procedures.

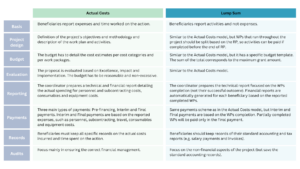

We summarise the main differences between these two funding schemes in the following table.

Understanding the distinctions between Lump Sum and Actual Costs funding schemes is essential for confident participation in different types of calls. While each model presents unique benefits and challenges, careful planning is key to building a successful proposal and ensuring its effective implementation.

Syntropie can be an invaluable partner in EU-funded projects, offering expertise in project management and developing communication, dissemination and exploitation actions. By partnering with us, you can leverage our experience and skills to maximise the implementation of your Lump Sum project.

Would you like to have an expert to support you in setting up your winning Lump Sum proposal? Contact our partner Efund.